Do you get tired of paying that monthly mortgage bill, knowing you have years and/or decades to go before paying it off?

Do you cringe when you see that most of that payment is going towards the interest?

Well, I have come up with a plan that I know will help you pay off your mortgage quickly.

Disclosure: Some of the links below are affiliate links that I have provided for your convenience. Click here to read my full disclosure policy.

Disclosure: I am not a financial planner or advisor. I just know what worked for me and want to share the tools I used. If you have questions about financial planning, please seek advice from a licensed financial planner/advisor.

Update

As of March 2020, we paid off our mortgage!

It was not easy, and we had to sacrifice some things here and there, but we did it.

How This Plan Came About

In December of 2012, repayment of my student loans began.

I was to pay close to $600 a month for the next 10 years. WHAT!!!

And I am sure others have worse payment amounts.

I needed to come up with a realistic plan to get rid of this debt.

I got out a pencil and paper and got to work.

Happy with my plan, I immediately put it to use, and it worked!!

I took on a 10-year debt and paid it off in 37 months.

It was the success of this plan that motivated me to apply it to our mortgage.

Creating a Plan for Your Mortgage

Before you begin to pay off your mortgage, you must pay off all other debts first.

The beauty of my plan is that it can be applied to any debt, so follow these steps for all your other debts first, then work on that mortgage.

Another requirement is that you do not take on any more debt if you can help it.

That is, do not buy a new car just because you don’t want your old one.

If it runs, keep it ’til that baby dies or at least until you finish paying all your debts.

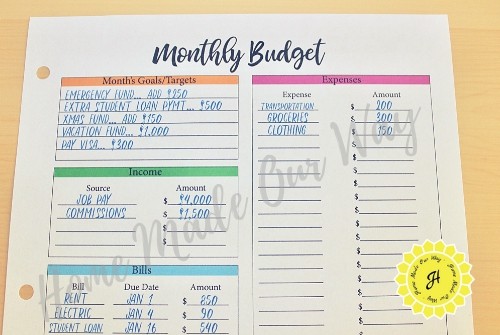

Budgeting

First, go over all your finances and create a budget.

You cannot skip this step.

You must become aware of your finances, your ability to save, and your spending habits.

If you are ‘horrible’ with money, this is the time to learn.

You need to commit to your finances to put a plan in place.

To help you put a budget together, visit the following site: Money Helper.

This site will help you set up a budget and create a plan to help manage your finances.

If you do not like using a digital budget maker, try our finance planner pages.

In it, you will find everything you need to help get your finances in order.

Just click the button at the end of this post to get your free copy.

Setting Up Goals for Your Mortgage Plan

Next, with your budget completed, make a note of all your debts (loans, mortgages, credit card balances).

Find the debt with the highest interest rate (do not include the mortgage unless it is your only debt) and create a goal plan.

I love Bankrate.com because they have a variety of calculators that you can use to help create your plan.

The best thing is that it’s free to use.

Click here to access Bankrate.com.

After you have created a budget, you will need to calculate a minimum amount that you can pay in addition to your regular monthly payment.

Depending on your bills and your willingness to cut back on some of your expenses, this amount may vary.

I was able to commit to $200 a week to pay off my student loans.

So, come up with a doable and reasonable amount.

Now, you need to pick one day of the week on which you will make your payments.

That’s right. You will be making weekly payments along with your monthly payment.

For example, I made payments towards my student loans every Monday without fail.

Setting a Deadline for Your Mortgage Plan

With your minimum amount on hand, go to Bankrate’s calculator for your debt’s amortization table.

Enter your monthly and extra payment amounts in the boxes provided to calculate your goal date.

You should then be able to print out your debt’s amortization table, which you will use for your plan.

After creating your goal plan for this one debt, stick to it and continue paying off your debt to meet your goal deadline.

Make sure you enter this debt’s weekly payment into your budget and planner so that you don’t forget to pay it.

Keep your plan in plain sight so that it is always on your mind.

And when you make a payment, cross it off your amortization table.

Paying It Off More Quickly

Now, don’t forget that you have entered a doable and reasonable minimum amount, but that doesn’t mean you can only pay that amount.

If your budget shows some ‘extra’ money, then put that amount towards the loan.

If you get a tax refund, consider putting some of this money towards the loan.

Even though I committed to paying $200 a week, I would usually pay more than that, which is how it went from a 10-year loan to a 5-year plan to getting it paid off in 37 months.

If Your Mortgage is Your Only Debt

When going over your finances, make sure your mortgage does not incur pre-payment penalties.

If it doesn’t, then go for it.

Also, call your lender and make sure that you are paying the lowest rate to which you qualify.

With all your other debts paid off, it’s possible that you will have a high credit score making you a great candidate for a lower rate.

If the rate is very low, check all your options for loans with a 30-, 15-, or even 10-year rate.

The shorter the time, the lower the rate.

Why Pay Off Your Mortgage Quickly

You are probably wondering why I am trying to pay this mortgage off or why should you.

Here are some good reasons:

- Become debt-free

- Save more of your money by paying less interest

- Help you save faster for other things like a car

- Help you save for retirement

- Avoid having a mortgage when you retire

- High credit score

All these reasons kept me motivated.

However, when I started this plan, I questioned my methods and wondered if I was doing the right thing.

You hear about things like “good debt vs. bad debt” or “one should fund their retirement accounts to the max before paying off things like a school loan or mortgage.”

But I kept thinking: why should I continue to owe money plus interest if I can get rid of it for good?

Then, last month, I read an article by Michelle Singletary, a financial advisor whose columns can be seen in the Washington Post.

In it, she wrote about the very things I have been doing.

She touched upon the importance of becoming debt-free.

She advises people to pay off their mortgage before they retire, making it one less payment to think about every month.

If you’d like to read Ms. Singletary’s article, click here.

I hope it inspires you to become debt-free as well!

Additional Help

Need help with your school loan debt before paying your mortgage off? Click the link below.

Free Financial Planner Pages

Click the pink button below to get your free financial planner pages.

Leave a Reply